Chapters

Show Highlights

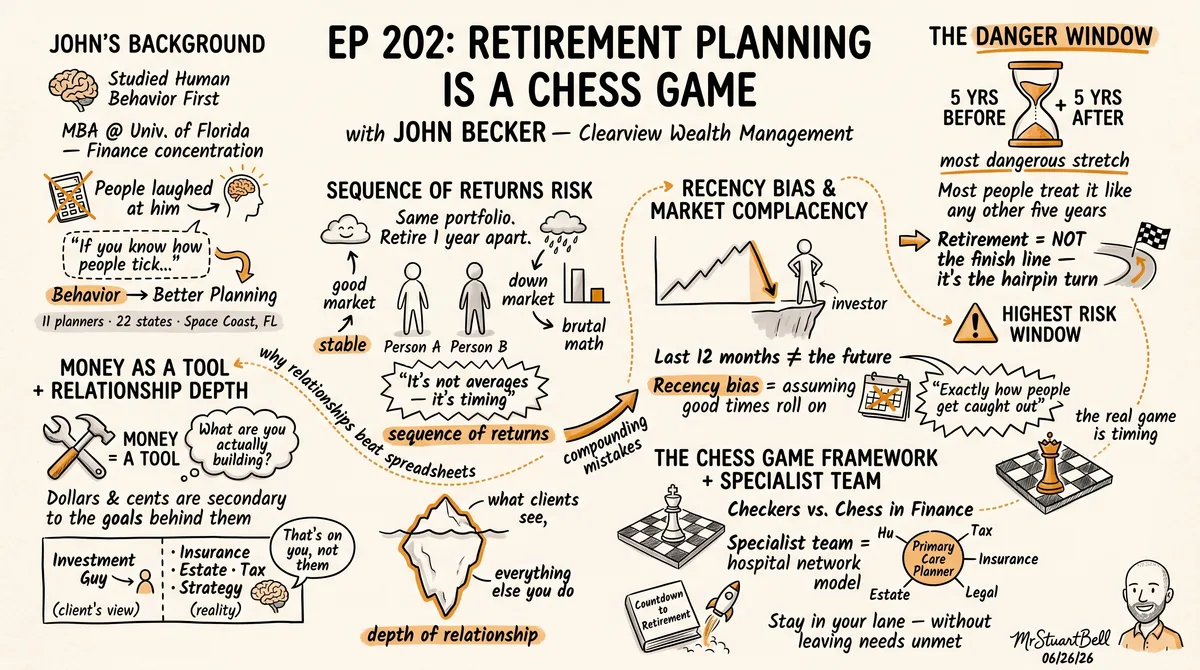

- The five years before and after retirement are the highest-risk window in someone's financial life, and most people treat them like any other five years.

- Sequence of returns risk means two people with identical portfolios can retire one year apart and end up in completely different financial positions.

- Recency bias makes investors assume the last 12 months of market performance will continue indefinitely, which is exactly how people get caught out by downturns.

- If your clients only describe you by one service, that's on you, not them. The relationship wasn't deep enough to surface everything else you do.

- Building a team around specialist expertise, like a hospital network with a primary care physician at the center, lets you stay in your lane without leaving client needs unmet.

- Money is a tool. Before you can plan well, you need to know what the client is actually building, because the dollars and cents are secondary to the goals behind them.

John Becker founded Clearview Wealth Management on Florida's Space Coast and now runs a team of 11 planners covering clients across 22 states. His background isn't what you'd expect. He came up studying human behavior before pivoting to finance, and people laughed at him for it. That background is exactly why his approach works.

What I found most interesting talking to John is how he thinks about the retirement window. Most people treat retirement as a finish line. John treats it as the most dangerous stretch of the whole race. There's a concept called sequence of returns, and if you retire into a down market while drawing on your portfolio, the math gets brutal fast. It's not about averages. It's about timing you can't fully control.

He also makes a point I've seen play out after more than 1,200 books. Clients often only see one slice of what you do. John's clients call him their "investment guy" when he also handles their insurance, estate planning coordination, tax strategy, and more. That's not their fault. It's a depth-of-relationship problem.

John's got a book out called Countdown to Retirement, and this conversation covers the thinking behind it. If you work with clients who are five to ten years from retirement, or you're in that window yourself, this one's worth your time.

Transcript

AI transcript provided as supporting material and may contain errors.

Stuart: Hey, everyone. Welcome back to another episode of the podcast. It's Stuart Bell here, and today joined by Jon Bechtoll. Jon, how's it going, buddy?

John Becker: It's doing wonderful, except for the sunburn.

Stuart: I'm up in Pennsylvania, most people know. You're actually down close to where the office is. You're in Florida, right?

John Becker: Yeah, we're over in the Space Coast. I always say Space Coast, 'cause some people, they hear Merritt Island, they go... have no clue where that is. Then when I say Cocoa Beach, the shuttle system, Melbourne, Florida, they go, "I think I know where you're talking about."

Stuart: Slowly dial it in.

John Becker: Yes. If I say the greater Cocoa Beach area, most people have a g- a, a vague idea what I'm talking about.

Stuart: They, everyone should know that area explicitly, because there's a place down by you that's called Stuart, spelt the correct way. ah,

John Becker: yeah. It's about an hour and a half south of us, but yes, wonderful town.

Stuart: I'm excited by this show, 'cause we're gonna share some of your approach with people. And what's really great about the podcast that we've done recently is really trying to communicate to people that everyone's got their own expertise, and for one person, that might be relevant to 10 people, and for someone else, it might be relevant to 10,000 people.

Stuart: But your audience is your audience, and just- the numbers are irrelevant. If you can talk to the people that you want to talk with, then that's the most important thing. So this is gonna be a good example of that because your subject, as we'll get into, is relatively broad. but the way that you approach it is relatively specific, or the conversations that you're having is relatively specific.

Stuart: So this is gonna be a nice bridge into that. So why don't we start, give people a bit of background, what it is that you guys do, and we'll go from there.

John Becker: Yeah. So I'm the founder of Clearview Wealth Management. in a nutshell, we are a financial planning firm. as of right now, 11 financial planners and four support staff members.

John Becker: And if you can envision the state of Florida, we pretty much cover the I-4 corridor from Melbourne heading west into Orlando, heading into the greater Tampa area. but we actually have clients across 22 states in the union. we also have quite a few dual citizenship clients as well. But, yeah, that's us in a nutshell in that respect.

John Becker: most of our expertise lies in financial planning, investment management, retirement planning, and also housing insurance and other holistic needs as well. we don't... We're not actually attorneys, but we do engage in the basics of estate planning and kind of helping educate clients to get them a little bit better organized for when we are also working with their accountant or their attorney, and that way do we have the, what I call the triage of the A's, the advisor- accountant, and of course the attorney. And hopefully they don't have to deal with the attorney too frequently other than- ... done. But, people that have special needs trusts or sadly they've, they're going through a divorce or something that, there's gonna be a little bit more hands-on and a lot more communication for that part of the quadrant.

John Becker: Accountants you can That's- ... hear.

Stuart: Yeah. Yeah. Yeah. It's the more regular touch points. That though, I think is the, It's easy to think of what we do in silos and forget about the touch points from the client's perspective that whatever we do touches upon or impacts or has some kind of need from or push to.

Stuart: And I think it's really interesting where we are now. we're recording this at the beginning of '26. There's lots of, hand-wringing and hair-pulling about AI taking over different industries and, humans getting sidelined in different ways. But I think for anyone who's just on the execution side, if a robot can do the job, then that's a risk.

Stuart: But our expertise, the expertise that you just talked about, being able to see the connections that aren't necessarily directly to do with the work that you do, but adds value to the client, that's where some real benefits come in.

John Becker: Yeah. When you start talking about someone's, actual goals and objectives, not just the dollars and cents of it, 'cause I tell people money is a tool.

John Becker: You need a screwdriver and a hammer to build a house, but the house doesn't build itself. So we need to get, like, where... what really matters to you. what kind of legacy do you wanna leave behind? how do you feel about the markets? all those types of things.

Stuart: And shame on us sometimes because some clients, they'll go, "Oh, he's my investment guy." we do all these other things, too. And then sometimes people go, "Yeah, he's got my home and my auto insurance. He's a great guy to deal with." I'm like- I do all these other things too, but that's shame on me, like for not getting a little bit more of that depth of relationship with that client because obviously they know, and trust me, so why aren't we handling all of things for them, Yeah.

John Becker: That's why we have the expansive team that we have. It's not just the geographic territory, it's also the different levels of expertise and, actual, how to put it, their dedications to a certain element of financial planning. Because, you can really be, a jack of all trades and a master of none if you're really not careful.

John Becker: I like to think of myself as like a primary care physician, where I have a very broad knowledge of all these things, but if you start getting into the weeds about Medicare, m- m... I'm not your dude, But I have- Yeah ... someone to talk to who is. Robbie Rosenberger, who we're also co-authoring the other book with, his dedication is really fixated on small business owners, how to help them not just with the financial planning, but how to actually become more efficient, how to make their business more attractive to a potential suitor.

John Becker: how to wander in the weeds if it's a closely held business and weird fi- family dynamics. I'm not an expert at that. I know enough to be dangerous, but that's why he's there. He's my cardiologist, if you will, Yeah. He is the, a little bit more keen on estate planning, so he would be our, our pediatrician for the kids and the grandkids.

John Becker: You know what I mean? Like-

Stuart: Yeah ...

John Becker: so it, it's like running a hospital network as much as it is, like a financial planning network,

Stuart: And understanding where those touch points are, like as the advocate for the client, as the primary physician understanding the bigger picture and then knowing what's in your immediate sphere of influence and then what to refer out in network and then out of network as well.

Stuart: That expertise, the ability that you've got to make the relationships and see through the surface level details to what's really making a difference, I think as most people are listening to this, most of the clients that we've worked with in the past, none of us are just transactional, quickly sell something and then onto the next.

Stuart: We're all in relationship businesses, and those relationships come from something a little bit more meaningful than just checkbox exercises.

John Becker: I agree. I mean-

Stuart: Yeah ...

John Becker: a- and it's also, I've also seen in my industry, you see the term financial planner or financial advisor thrown around very easily and loosely.

John Becker: But I also see a dynamic where if I go to see certain advisors at certain wirehouses, they're investment guys or gals only. You start talking about long-term care insurance, home and auto insurance, life insurance, tax management, estate planning- It's all about rates of return and beating the market and that kind of stuff, which I love talking some of that stuff too, but it's not the big picture.

John Becker: You know what I mean? Yeah. It doesn't... for all the what ifs that, happen to most of us.

Stuart: So that's an interesting bridge into the clients and how they find you and what resonates. Yeah. The wealth planning, retirement management type industry, there's typically like the accumulation phase and then the retirement and the drawdown phase.

Stuart: Do you guys specialize in, or even not specialize, but tend to work with one group more than the other?

John Becker: that, that kind of is what turned into the book, interestingly enough, Countdown to Retirement. I would say the mass majority of first meetings with an initial client or a prospective client, it seems to be like this interesting window of they're either within a few years of retirement or they're in the first few years of retirement.

John Becker: And as we get into in the book, those are actually the most vital years to get right, in terms of... I don't wanna say market timing, but there's a term that we reference that some of you may be familiar with. Sequence of returns. Yeah. So for... someone goes, "Okay, if I just put all my money into the S&P 500," the big, broad index of the stock market in the US, "I will make a- on average 10% a year, so I'm just gonna swing for that."

John Becker: And I go, "Okay. here's the good news. If it was the last five years and you're retiring today, you're a genius."

Stuart: If it was

John Becker: the year 1999 and you're retiring in the year 2000, and you invested all into the S&P 500, you almost lost half your money. Plus, if you retired, I'm assuming you're drawing on that money too.

Stuart: I-

John Becker: it's not a matter of averages, it's actually a matter of what are you doing for all the ifs to try to smooth out the ride. And, from an investment management standpoint, that sometimes is easier said than done. Yeah. I... people are getting complacent right now because, the last few years, 2023, 2024, and 2025, double digit gains each year.

Stuart: People's memories are short, right?

John Becker: There's a... What's the psychology term? Recency bias.

Stuart: Oh,

John Becker: People have a tendency to think in terms of no more than, say, six to 12 months in the past and presume that's what the future is moving forward.

Stuart: Yeah. A

John Becker: lot of people that made that mistake in the year '07.

Stuart: Right.

John Becker: 2008 was the great recession. And- ...

Stuart: and like you said, the sequence of that, although the averages in a infinite timescale build out, but you are anchored to a particular point in time, which I think is interesting about your industry because- What would be similar, I guess kind of health events are out of your control.

Stuart: When it happens.

John Becker: What I was talking about earlier, man.

Stuart: Yeah.

John Becker: Yeah, I made double digit gains every year. Rock and roll. And now we're into a down year, and now you're going to a nursing home. Now what?

Stuart: Yeah. Yeah. There's other industries where it's less. Like even moving house, there's... Some of it is discretionary, some of it is forced, but probably a lot of it's discretionary.

Stuart: Non-critical medical procedures, if you do it this year or next year, okay, maybe not the same. So it's really interesting having this extra dynamic of a transition point that is a window that closes for people, and something's gonna happen, so they can either proactively make those decisions or the decisions hap- happen to them.

Stuart: Yeah. When you're talking with people, do they realize that? Or are people typically coming in relatively cold and, "Hey, I'm at this point. I know I need to do something, but I don't really have a concept of what the something is."

John Becker: this is a term that I know a lot of clients hate to hear on a first meeting, but the two words are it depends.

John Becker: I will say there's sometimes a little bit more of an emotional attachment to someone's portfolio as a nest egg. people have, mental milestones. "Oh, if I hit 2.5 million, I'm good to go for life." It's have you factored your longevity? Have you factored inflation? Are you too conservative?

John Becker: Are you too aggressive? and then some people, they get a little bit more logically driven, but then there may be some fallacies behind it. So for... A good example would be someone comes in with a portfolio and says, "Okay, I hit three million. I just wanna move it to money market or ladder some CDs, 'cause I think I can get 4%."

John Becker: And I go, "Okay. what happens if the Fed cuts rates?" Is that a problem? I'm like, because rates wouldn't be 4%, they may be 3% or 2.5%. In fact, if you go back to even just COVID, a lot of CDs were 1% or less.

John Becker: So w- what are you gonna do? You're gonna eat into your principal. then have you factored inflation?

John Becker: Have you factored requirement of distributions? I think sometimes people almost get caught in a game of checkers when personal finance, and especially when it comes to variables like the markets, it's more of a game of chess.

Stuart: Right.

John Becker: To be an expert, but you need to at least have an open mind to someone that deals with it day in, day out.

Stuart: That what if, I think being the insider, seeing it day to day, knowing what all of the moving parts are, being able to go to someone with that what if, and thinking that, what principles are applicable to anyone listening, and I think it's broadly the same for most of us. Again, on the assumption that we're in a relationship-based business, we're not in a kind of a checkout consumer goods type thing, just a spur of the moment purpose, then the knowledge that we've got is the expertise that people are really buying even more so than the execution.

Stuart: the execution, it's almost table stakes. Everyone assumes that you can do the job. So it's then the expertise that you bring to it. So thinking about that expertise that you've got and sharing it with people, do you typically find that, people are open and resonate with the ideas that you say, or do most people come with fixed ideas and then it's a re-education exercise?

John Becker: I would say it works like this. Most people that we encounter for a first time are gonna be married, for the most part. Usually husbands and wives or wife and wife, husband and husband for, the gay community, usually one has a different mindset when it comes to money than the other. the key is to work in a collaborative nature and try to find a way to compromise what's the middle ground that we can find together as a team, knowing full well that essentially the fact that they're even sitting with me looks like to me that they're trying to find a captain to the ship.

Stuart: Right.

Stuart: And

John Becker: be the ship hands, and they don't fully trust themselves to be steering at the helm.

Stuart: Yeah.

John Becker: otherwise, why are you meeting with me to begin with? It means that you're open to it, so then sometimes it might be a matter of they would rather just do a fee-based financial plan and say, "Okay, I need someone to lay the blueprint for me objectively that really knows this stuff, but I still want to man the helm myself."

John Becker: That's fine. But I would say about 90% of our clients, if they're willing to sit with us and open up like that, they are looking for someone else to helm the ship, not just lay the blueprint or map out- Yeah ... the years ahead. For the most part.

Stuart: The, this idea of the amplified expert, the expertise that we've got of sharing it with people in the most effective way, it's so interesting because in isolation we get in our own heads about the bits and pieces that we know, particularly on small business owners because we're typically dealing with the more difficult cases, the edge cases, the random things that don't come up, and we f- it's easy to forget sometimes, unless we're face to face with clients often, it's easy to forget the conversations that they're having are often more basic.

Stuart: The questions are five levels below where we're typically operating because they're the introductory level questions. So this bridging your advanced knowledge into the more straightforward questions, do you tend to find that typically there is a set of five or six questions that everyone asks some variance of, and then the edge case stuff is really on the long tail of random questions?

John Becker: there, there's probably a little bit of gender bias. put this very delicately, I would say women that are engaged in financial planning with us, they're a little bit more goals and objectives oriented. and men sometimes are a little bit more sometimes overly logic driven, and they're a little bit more centered on how do you get compensated?

John Becker: Meanwhile, women are a little bit more focused on what's gonna be the nature of our relationship? How's our communication gonna be? What's the frequency of our communication? but the most common between both is definitely, how do you get compensated? What's the difference between a fiduciary or a broker?

John Becker: That's a very common one, and it sounds like semantics too when we talk about it, but there is a very clear distinction. a broker just needs to do what's suitable. A fiduciary has to do what's in your best interest. doesn't mean they're gonna get you exactly everything that you wanted.

John Becker: They're just gonna put in the most educated guess that they can possibly put together for you to put in place, and it's totally in your best interest from an objective standpoint. Doesn't mean it's always gonna be the right call, but it's as good as it can possibly get without just- Yeah ... being about compensation.

John Becker: the other one that's really interesting, and the questions have actually diluted over time because a lot of our business is actually referrals So it usually ties into, "Hey, you did this for my sister. I want something like that." And then it's like I have to go, "Okay, let me expand some questions-

John Becker: to get focused on you," because I can take 100 people that were born on the same day with the same health history and everything else, and there's probably gonna be 20 to 30 different combinations of solutions- Oh ... to come up with. Yeah. 'Cause their risk difference isn't the same, their focus on the markets isn't the same, their concerns about what keeps them up at night isn't the same, their feelings on life insurance isn't even the same,

John Becker: the... I don't think people realize and can really stomach, like, how different they really are deep inside. And

Stuart: so-

John Becker: from the person next to them ... they did with their finances. And money do- isn't everything, but dear God, life without money is very probing and difficult.

Stuart: And people get very vested in their outcome.

Stuart: Like you say, it's got such a consequential impact on every other decision- ... that it really makes it a big deal for people.

John Becker: Yeah. And some people could care less about the what ifs. They just go, "Just make me the most money you can possibly make me, and I'll figure out the rest." I will say those relationships usually aren't long-lasting.

John Becker: 'Cause they don't have a hol- a holistic mindset.

Stuart: Yeah.

John Becker: But I also always need to help and focus and reassure folks that maybe we need to put the horse blinders on a little bit, because you have too many variables in your head and it's causing you anxiety, ... going back to small business owners, it's not exactly the same, but you'd be surprised how ingrained a lot of small business owners are with their business, to where sometimes they just have, a mental math of what their business is worth without actually properly doing the valuations.

John Becker: Because sometimes it could be worth way less or way more. And I make the joke to a lot of small business owners that, employees and entrepreneurs are two different worlds. But if there's one thing that you should probably get at least a little bit in your mindset, most employees that are planning for retirement are contributing to a 401.

John Becker: Small business owners should have similar products as, as well, but what is the biggest source of wealth for the employee? Their 401and their house, right? Okay. Small business owner, you have to start thinking in terms of your small business as like your 401, but you can't just go on an app real quick and see how much is in your account right now.

John Becker: But you need to at least look at your blueprint periodically to really know, "What's my price tag?" Because what if, by the grace of God, one of your old colleagues comes around, says, "Hey, let's go grab a drink. By the way, when are you selling your business? 'Cause I'd offer five to six million within a few months if you'd be willing."

John Becker: you better know that price tag in your head on the spot because who- who

Stuart: knows? Yeah

John Becker: Maybe

Stuart: you don't get the

John Becker: offer again.

Stuart: At least have a ballpark. Yeah. We did an evaluation in Spork recently, and the person was joking saying that ask the same person what they think their business is worth if they were to sell it, and what their business is worth to the IRS, and those numbers were very far apart.

Stuart: And the truth is probably somewhere in between. But that idea that people's mental hooks on even the same subject, but change the context and they would give two very different answers, so let alone all of the other nuanced elements of- of retirement.

John Becker: I tell small business owners and individual investors the same thing.

John Becker: It's not what you make, it's what you keep that matters. If you're averaging 10% rate of return but you're not tax efficient and you're really only keeping seven, wouldn't you rather have eight and keep eight?

Stuart: You know what I mean? Yeah,

John Becker: yeah. Very simplistic, but really tax drag is a huge thing that investors and small business owners don't really stomach properly to really go, "Oh wow, I could probably be doing better just by keeping more of what I'm making."

Stuart: Yeah. And then that nuance comes in, like you were saying before, the complexity can add to anxiety. So I think a lot of our job is managing that psychological element of getting to the customers, getting customers to the place that they want to be, which ties back into the messages that we're putting out there.

Stuart: So linking this back to the book that you guys have just wrapped up, the Countdown to Retirement, I like the specificity of that because wealth management, retirement planning, there's more than one person doing it. The- the uniqueness that we have in this isn't necessarily the- the tools and services, it's the way that we bring it together and the relationships that we build.

Stuart: So that particular book, you guys are on the Space Coast, there's a lot of engineering space related people- Yeah ... out there. So as a campaign tool, Countdown to Retirement plays on those languages a little bit and- and adds to that, or allows for that jumping off point in the conversation. So talk to me a little bit about what went into the book and deciding what to include and- and what the main talking points were.

Stuart: I think a lot of people, again, we've got so much knowledge in our head as the experts, how do we distill that into something that's- that's useful?

John Becker: and you don't wanna paint so broadly that you're pigeonholing everybody into the exact same circumstances. But I think each chapter, we kinda touch on some areas that seem to be some of the most common concerns that bubble up.

John Becker: sequence of returns like we were talking about before, optimizing your returns without getting your face ripped off when the market declines. Because it's gonna happen at some point. and law of averages says this: if you're within five years of retirement or the end of five years into retirement, at some point you're gonna have a really nasty decline in the markets overall.

John Becker: How are some ways to psychologically prepare for it, but also, tighten up the ship, so to speak, so we are-

Stuart: ...

John Becker: able to navigate choppy waters when they come, because it's not a matter of if they are gonna come, it's a matter of when they're gonna come. there's always black swan events.

John Becker: There's always a 9/11. There's always, God hopefully hoping this doesn't boil over into more, but what's going on with Iran right now.

Stuart: Yeah.

John Becker: At least one event per year that could escalate into something far worse. And four out of five times it doesn't, but that one out of five, that's the doozy of them all.

John Becker: so we really focused on that. And then also one area that I haven't seen really addressed as frequently, at least not in literature. There's a lot of research paper on it, but clients and prospective clients generally don't read a bunch of research papers. Long-term care planning, and the term I use with clients a lot of times is the domino effect of long-term care.

John Becker: So nine times out of 10, this is what happens. You have a retired couple, husband declines, wife starts taking care of him, husband dies, wife is on her own. She's either unfit physically or mentally to take care of herself, and she's either going into assisted living or a long-term care facility for several years, drains their assets down to next to nothing, and/or has to move in with one of the children.

John Becker: If a person's in their mid-80s, how old are their children usually? In their mid, late- Yeah ... early 60s. What are your prime earning years as a worker? Those same years. So now you're putting your life on hold to take ca- care of mom and/or dad, and now those are your prime earning years where you should be really juicing up your retirement savings most likely.

John Becker: your kids are out of the house. You're... Hopefully they're no longer on your dime. the bank of mom and dad is your- ... hopefully has been shut off and they're doing their own thing So now all of a sudden, all this wealth that should be accumulating during that period is put on hold to take care of mom and dad.

John Becker: There's maybe a little bit of a wave of inheritance, but it's not enough to reiss- reshore up what could have been made during that time period. So guess what happens? That late 50s, early 60s child, they bury mom and dad, they're heading into their retirement with probably less than what they probably should have had, and guess what happens?

John Becker: The domino effect continues.

Stuart: It's such an interesting... we've worked with, coming up on 1,300 books now, we've worked with a lot of financial advisors. But that domino effect, we often hear about bucket strategies and all of the more traditional stuff that you hear about. But this is actually the first time I've heard anyone talking about that stacking effect and the consequence of that timing.

John Becker: I'm not explicitly saying everyone needs to buy a long-term care policy. That's not what I'm saying at all. What I'm saying is that-

Stuart: Be aware of it ...

John Becker: there's a very strong chance that if you're a married couple heading into your 60s, that one of you is gonna have a long-term care event. The thing is that it may not send you to an assisted living facility or a long-term care facility, but someone's gonna be stepping in, and it's usually your spouse and/or your children.

John Becker: So just plan for it to some extent, not only from an estate planning standpoint, having a medical surrogate or a medical advocate, depending on what state you're in, having durable power of attorney so at least they can take care of bills and stuff on your behalf without a lot of trouble.

John Becker: Because once you're deemed incompetent, there's no going back. You're dealing with the state. earmarking a little bit of money here and there, maybe doing a little bit of Roth conversions and just setting that money aside as, a hedge or, again, maybe looking at, long-term care insurance.

John Becker: Or I also find that a lot of folks, especially those born in the '60s and '70s, a lot of them bought, old whole life policies that have a decent amount of cash inside them. Insurance companies have definitely gotten a little bit more on the bandwagon of, hybrid products to where maybe it's life insurance but it also has, some kind of long-term care or chronic illness feature.

John Becker: Who knows? Maybe you've got enough in cash value where you can have, a self-funded or a low premium on something like that.

Stuart: Right.

John Becker: Your hedge. At least address it, Yeah. the... It's probably gonna happen, so why stick your head in the sand, I guess- Yeah ... is the point. So plan accordingly.

Stuart: That element of at least dress- address it, the no option isn't... There's no such thing as, a null option where there's zero consequences. The do nothing option has consequences. So at least if you choose to do nothing, at least you've chosen to do nothing.

John Becker: As long as you've done the math behind it and you're okay with that risk, so be it.

John Becker: I mean-

Stuart: Yeah ...

John Becker: there's gonna be risks you take, not just markets- ... but al- you know, lifestyle, driving patterns, whatever else may have you. Everyone takes some degree of a calculated risk at some point in their life.

Stuart: Yeah.

John Becker: You wanna do the calculus before you just accept it.

Stuart: before something happens.

John Becker: Yeah,

Stuart: exactly. This, I often talk to people about the idea of to a certain degree we need to sell people what they want and deliver what they need, maybe not in terms of products, but in terms of, messaging. So people's conversations will be here, and then what they actually need is here, and then we're trying to bridge that gap and close the Venn diagram across the two.

Stuart: For you guys in this industry, obviously some of them it's more separate than others. For you guys and the customers that, clients that you're dealing with, is that crossover a lot more? So a lot... People are more aware of what they want, so as you're talking about messaging and the information that you put in the book, you can be a little bit more explicit and it's a small step towards the outcome?

Stuart: Or is it that they've got very disjointed ideas from what the reality is, so you've got to kind of position things in this slightly s- disjointed place and then take people on the journey?

John Becker: All of the above. it kinda goes back in line with the idea that there's just so many different personalities-

Stuart: Right

John Becker: that, h- how to put this. One of my, when I was actually an undergrad, I actually had majored in psychology.

Stuart: Nice ...

John Becker: and I know a lot of people would go, "What the hell does that have to do with finance?" And I go, "You know, when I pivoted and decided to go back to grad school to do my MBA with a concentration in finance at University of Florida, I got laughed at by so many people."

John Becker: They're like, "That is the dumbest thing I've ever heard." And I go- ... "You know what? You may be right." But then when I actually, uh, decided to go become a financial planner instead of being an investment analys- analyst elsewhere, I found that, you know what, if you know how people tick, and you're willing to get into more a relationship mindset and really focus in on, like, what, what drives their decision-making process, it actually matters almost way more than the dollars and the cents and what- Right

John Becker: funds and ETFs really matter most. Those are analytics that can be done behind closed doors, behind a curtain. At the end of the day, most people don't really want... How to put the analogy. People are coming to you to say, "Hey, I really need a watch." "Okay. Tell me more about what style you want. Do we have a budget in mind?"

John Becker: Those kinds of things. When you finally present the watch that you think is a good fit for they usually don't care about how many cogs are in there or h- what the battery life and expectancy is. They just wanna know, okay, it's a watch. It works. Can you tell me a little bit more about the history behind it?

John Becker: But that's about it.

Stuart: Yeah.

John Becker: Coming to you for that kind of guidance anyway. So sometimes you don't wanna get too caught up in the minutiae. you really need to get more focused on the behavioral finance elements than the actual analytics behind it sometimes.

Stuart: Yeah.

John Becker: Your point before, it's like- are the Venn diagram, if you will.

John Becker: You have to be able to take analytics and a little bit of, for lack of a better term, salesmanship because essentially you're not necessarily trying to sell products per se, but you're selling your ability to really understand what makes them tick and how do you shore up and compromise a portfolio of investments and/or insurance products that meets as many of those goals and objectives as is actually feasible.

Stuart: Yeah. And to your point on the psy- To your point on the psychology piece, you're almost having to sell them on the idea that they need to do something. it's almost a motivational coach as, as much as it is a technical analysis.

John Becker: Oh my gosh. Oh, yeah. Sometimes you, sometimes, when... this past week has been a pretty good example, like people freaking out a little bit about the conflict in Iran.

John Becker: You have to realize these people, you're managing their entire livelihood.

John Becker: And when they hear doom and gloom on the news, sometimes they're able to just dispel it and go, "You know what? That's not that big of a deal." But when you hear about major events that could be that black swan event like we were talking about before, they need to...

John Becker: some reassurance from you like, "Okay. John, give it to me straight. How bad is it?" And then lay out the groundwork. And I don't want to be vague. I go, "Hey, based upon my presumptions of what's going on, based on the information that's at hand, here's what I suggest we do."

Stuart: Yeah.

John Becker: However, let's set some milestones.

John Becker: If by Easter Sunday this hasn't happened, maybe we need to pare down our risk, or if this has happened by this date- We need to rebalance and actually re-up our risk because our portfolio, the really conservative stuff, may take over too much of the aggressive stuff, and you don't wanna miss out on,

John Becker: the worst of times are followed almost immediately by the best of times when it comes to the market.

Stuart: Right.

John Becker: And I always try to tell people, "You don't time the market, the markets time you."

Stuart: It's interesting-

John Becker: Those best 10 days of the last decade-

Stuart: I was just gonna say you're timing- ...

John Becker: you actually decrease your annual rate of return by almost 2 to 3%.

Stuart: It's insane, isn't it? When you see the actual numbers that underlie and think about trying to time things specifically, the risk of missing out even a tiny number makes such a big impact.

John Becker: And that's why I try to create balances that are more in line with the best of times and the worst of times, but having the flexibility to pivot towards each.

Stuart: yeah. That-

John Becker: it's a, it's an art, not a science, though, sometimes. I

Stuart: will- Yeah, ex- ...

John Becker: it is an art, not a science.

Stuart: And as you say, it's as much psychology as it is mathematics.

John Becker: Absolutely.

Stuart: That idea of we've got this knowledge, we know from experience what we wanna share with people, we distill it down into the group that we wanna share it with.

Stuart: We've looked at it from their perspective, so we're using the language that resonates with them. As you're taking people through the book and then into the next steps, how much of a... If someone were to read the book and then walk through the door, how much is that married up with their experience afterwards?

Stuart: The building blocks in place to make sure that it's a seamless journey. Was that a big thought process that went into it?

John Becker: I... How to put it delicately. I will be very blunt in my admission to the assumption that many people that haven't sat with us yet more than likely are not going to read the entire book in its entirety if they already intend to meet with us.

John Becker: but I will say if you're curious about meeting with us, you'll probably find that if you just at least read through, maybe not dig in too deep except for the sections that really jump out at you, "Oh, this is what's bothering me at night, this is what's keeping me up at night." Some of the other stuff you might be like, "Ah, I don't really care that much."

John Becker: But still stuff we think about. I would say it would probably be helpful 'cause a lot of the n- the pure verbiage of the book is really how we speak to most of our clients. And if it turns you off, you might find out, "What? These, this crew is not for me. This is not for me."

Stuart: Which is fine. better to- We're not- You don't wanna try and convert people

John Becker: hey, that's okay. and generally speaking, there are times where people need that help, and maybe I'm not that person that's gonna really, hit home with them. We do have other members on the team that are definitely unique personalities that may be a better fit. Or you're gonna find out you really shouldn't be with a financial planner at all.

John Becker: The fact that you're even reading the book would m- make me think that you probably at least need to have a, an initial consultation with one of us. Yeah. but going back into if you already intend on doing business with us, I think it would still be helpful because at least you get a little bit more of an idea as to why exactly are they asking these questions.

John Becker: And a lot of people have some presumptions of how certain elements of financial planning work, most of the time not necessarily by googling it themselves, because that is a Pandora's box- ... that you shouldn't really open. you'll find out the hard way you should either invest all your money in gold, the stock market is rigged, your 401is a disaster, you should put all your money into a life insurance policy.

John Becker: You will find a whole treasure trove of bad

Stuart: i- Bad research ends in cancer ...

John Becker: some good ideas, but you gotta filter from the bad ones. I-

Stuart: It's that difference between knowledge and information. they're both- yeah ... data's there, but it's,

John Becker: It's out there. But, sometimes it's not applicable.

John Becker: So I think that's what the key- Yeah ... trying to get some of that information and actually see is it even really relevant to you Yeah. I get a lot of the same questions about It seems to be like going back to the questions you had before. What are the most common questions? I would say it depends on which era you're talking about.

John Becker: I would say in the last three to four years, what are your feelings on Bitcoin and cryptocurrency?

John Becker: And then before that, what are your feelings on precious metals? It- there always seems to be like one or two like alternative investments that-

Stuart: Flavor of the month ...

John Becker: somehow the majority of people are fixated on.

Stuart: Yeah.

John Becker: Not to say that they're to be dismissed, but it's more I think maybe we're talking about something that may be 2% to 3% of your portfolio, not a

Stuart: hundred- Not the whole thing. Yeah ...

John Becker: so we're- That point- ... a little more, broader in our scope as opposed to the one-trick pony.

Stuart: Yeah. That point you were making about people, we've got a concept in one of our scorecards called Familiar on the First Call, so this idea that as people are consuming part or all of the book, and then when they turn up, they're turning up predisposed to at least have a meaningful conversation because they already like the...

Stuart: If they didn't like the, as you said, if they didn't like what you were saying, they wouldn't turn up. So it does a good job of kind of pre-qualifying to a certain degree people at least in the same ballpark. So do you have that feel for... The book's obviously new, so we haven't got direct feedback there.

Stuart: But do you have feedback from like referrals if people have meaningful conversations with the per- person that refers them, you can see that in those initial conversations?

John Becker: Yeah. So it, it's interesting. recorded a podcast with a regional director at Prudential Advisors, and it aired in January, mid-January, and I actually referenced the book and he said...

John Becker: we brainstormed almost in real time during the podcast. He's we're talking about, what a great marketing resource for gathering referrals. it was like almost not necessarily an epiphany, but it was more like, you know what? That's stupid not to do.

John Becker: okay, I'm sitting doing a review with a longtime client, and I admitted to I'm one of the worst people at asking for a referral outright. I get a fair amount of referrals just organically, but just asking for it- I don't know, just have never been that great at it. But if you say, "Hey, by the way, we just finished up this book," a lot of it's stuff that we've done together already.

Stuart: Yeah.

John Becker: Maybe someone you care about would see value in it.

Stuart: Yeah.

John Becker: And the funny thing is just in mentioning that podcast in the podcast, and then I sent the link to 50 of my closest clients who I also consider friends, I got three referrals within two weeks of the podcast coming out. And like there you go, because, how to put it?

John Becker: I don't really want to be one of those people that goes out seeking new leads. I like to do business with people I know, and trust already. So if it's referrals from an existing client, that's actually a little bit more in line with me, but I also don't wanna turn down people that really could use us.

Stuart: Yeah.

John Becker: And maybe I'm not the right fit, but someone on my team probably is.

Stuart: Yeah.

John Becker: Some- Like I said before, there's r- there's 11 of us, and we're still expanding. Maybe I'm just a personality clash or maybe I'm just not the right fit for you, but there's a good chance that if you need help, we got somebody for you.

Stuart: And that's starting that conversation with the book through a referral. So as they're talking, it's not just, "Oh, give me their name and email address and I'll call them." It's you giving them something to give to the other person. The whole kind of psychology of sharing value from the start, not asking for something from the start, it just makes everyone feel good.

Stuart: The person gets... You get to remember the opportunity to make at least a soft referral, they get the opportunity to give something of value to their person, the person receives something useful, and they're not just having to sacrifice the time before they're even sure it fits right for them. So effective.

John Becker: Yeah. There's the nature of reciprocity, right?

Stuart: Yeah. When

John Becker: g- How to put it? If you're a taker, you obviously don't understand this concept at all. But if you're a giver, a lot of people will say, "Okay, if you handed out 100 books but you only got 10 referrals, was it really worth it?" It's absolutely.

John Becker: 'Cause you know what? Yeah. At the end of

Stuart: the day.

John Becker: Those 100 people that received that book, and they're my clients, I almost... How to put it delicately without sounding weird? I've instilled in them a sense of confidence that they made the right call.

Stuart: Yeah. "This is

John Becker: my dude. This is the guy I call up whenever I have the most random questions about what's going on in the world, buying a new car, whatever."

John Becker: And I care enough to share it with someone else I love or care about.

Stuart: Yeah.

John Becker: It may not create immediate sales, but it is that sense of goodwill that's hard to quantify.

Stuart: And I think in... We were saying on our call the other day, I was just saying to someone else on the call before this one, that in where we are today, the signal-to-noise ratio that's coming from AI is moving more to signal and less noise because that, the robotic signal is getting increasingly better.

Stuart: But the moat that we've got as humans is to make that connection with other people. And exactly what you were talking about as far as referrals go, make feel good, make people feel good about it, deliver value first, resonate with that 10 in 100 people who are your audience, the people who will work well with you and you work well with them.

Stuart: That's the real opportunity that we've got, is to keep that human connection going and not just try and shout into the void and compete with all the noise. It's the opportunity to make those real connections with real people.

John Becker: even if AI develops real sentience, its ability to really connect the dots with the emotions is still gonna be very poor.

John Becker: Yeah. I actually see AI as a tool to help expedite processes so we can focus on the relationships more.

Stuart: Yeah.

John Becker: plug into AI your portfolio, and I compare it to what I usually would utilize, I can immediately find, downside risk, upside capture, all the analytics that I care about but most clients don't, and I can build that portfolio and use all these thousands of Monte Carlo simulations.

John Becker: It's beautiful. It really is. But if I have that trying to replace me in the relationship- I, this is not gonna be a client that ever wanted an actual financial planner. They just wanted-

Stuart: ...

John Becker: someone to plug in-

Stuart: A robo-advisor

John Becker: And- Yeah ... and I think the robo-advisors haven't taken over.

Stuart: Yeah.

John Becker: And interestingly enough, I, the research isn't quite there yet, in terms of law of large numbers, but you would presume, Generation Z, Millennials and whatnot would be more inclined to use AI instead of an actual financial planner.

John Becker: they're more inclined to try it, but interestingly enough, they still like the relationship. They like to sit knee to knee with someone who knows their kids and eventually their grandkids and eventually- Yeah ... carries the torch to that next generation.

Stuart: Still human connections, and that's the point of the book as a tool.

Stuart: It's a tool towards a conversation. We're not talking about books as the product. We're not talking about selling books or being a traditional author or just even doing it for the credibility auth- or authority. It's the opportunity to start the conversation, and a book is just a very effective way of starting that conversation meaningfully.

John Becker: The book will have checklists and, tools you can utilize to help frame your mindset towards financial planning, but the book is not going to tell you everything you need to do to retire. it's just not. No. Because too many people that may still have pensions, have different risk tolerances, have different health history.

Stuart: Everyone's an edge case, like you said.

John Becker: Everyone's a delicate, unique little snowflake, so don't- ... don't expect to wander through the blizzard with a 100-page book and solve all you need to know.

John Becker: no. That's not what it really is. It's more like how to frame the mindset and get into a financial planning relationship and have it have real impact, as opposed to you wander in blindly and you're just, almost like a sponge trying to soak in all this information.

John Becker: It's no, thumb through the book. the key areas where- This

Stuart: is the- ...

John Becker: concern and other areas where you just don't care.

Stuart: Yeah. Yeah, exactly. Fold down the important pages and- ... we'll talk more about that.

John Becker: And I also like to make the joke sometimes, and maybe it's a little colorful and disrespectful to some, but, I don't have a problem dragging an agnostic to church.

John Becker: someone that questions why we're even doing this.

John Becker: But it's really darn hard to drag an atheist. Do you know what I mean? If you've denounced the role of a financial planner, we're- w- don't... It's okay. Yeah. Moving... But if you question it and you're open to hearing more, that's the relationship.

Stuart: At least it's become a conversation.

John Becker: Yeah.

Stuart: Yeah.

John Becker: Not just speaking to just the true believers, Like-

Stuart: Yeah ...

John Becker: but there is i- it can get a little black and white in that situation,

Stuart: And you don't need to... I think for all of us, as we're thinking about the business that we're in, we don't need to...

Stuart: if our business was built around converting people who had already decided that it wasn't for them, holy cow, that's a uphill battle day after day. The benefit is-

John Becker: It's not worth it ...

Stuart: the... no. The world's big enough just to keep putting the message out there, your message, whatever it is, in enough places where it finds the audience, and then have an easy way for the audience to take that next step and knock on the door.

John Becker: Yeah, and I think there's gonna be a real ripple effect, too. like I was saying before, there's gonna be some goodwill that's not quantifiable. Yeah. But if there's a handful of people that I never even meet with that find that one little nugget that, like, all of a sudden it sends their entire family into better prosperity, all right, cool, man.

John Becker: Yeah. I, I-

Stuart: Good world ...

John Becker: maybe I'll get an attaboy from St. Peter

John Becker: sometime. You know what I mean? I like to think that. it's the pay it forward mindset. Like-

Stuart: Yeah ...

John Becker: maybe I don't see it for myself, but someone somewhere down the line got it.

Stuart: yeah.

John Becker: Me too.

Stuart: And that's the benefit. This whole idea about amplified expert and sharing your knowledge with people in a way that there is some downstream commercial benefit.

Stuart: But actually, it's also just making a difference in the world and sharing something that, as you said, even if you never see them, hopefully it makes someone's life better for one reason or another.

John Becker: Yeah. Isn't that a commonality whether it's... Just getting in the weeds a little bit. There's a commonality between Jews and Christians and Muslims and Hindis and Buddhists.

John Becker: Leave the world a better place than you found it.

Stuart: yeah.

John Becker: I mean- Yeah ... I think there's that commonality that, we should aspire to. you know what? Sending this message out there, maybe it isn't immediately financial gratifying- But there's probably gonna be enough goodwill that comes back from it to where maybe it changes my mindset.

John Becker: those down days where I'm like, "Why the heck do I do this to myself?" Folks, there are those days. I'm 15 years- Yeah ... deep and there's still those year, days where I'm like, "I, I don't know what I'm doing. Why am I doing this to myself?"

Stuart: Yeah.

John Becker: But maybe it's something like this that kinda goes, you know what?

John Becker: You're doing what's right, man Putting

Stuart: something good in the world. yeah

John Becker: You, doing all you can. All that you can do is all that you can do.

Stuart: Yeah. Yeah. Yeah. Exactly. Exactly. But I wanna make sure that we can share your details with people. Where's a good place if people wanna follow along with what you guys are doing, particularly, maybe they're in Florida or even out of state.

Stuart: What's a good place for people to go to?

John Becker: Yeah, like I said before, we serve more than half the United States, so we're not just here in Florida, but we do... If you wanna see us face to face, Florida's probably more ample. clearviewwealthmanagement, M-G-N, N as in Nancy, T.com is our website. we've got a bunch of resources on there.

John Becker: We also have downloadable articles we've written. There's some tools, some basic, retirement planning tools and stuff on there that you might like. And if you kinda wanna see a face to the names, it's ourselves as well as our support staff on there, as well as, a whole suite of the different types of services we provide folks.

Stuart: Fantastic ...

John Becker: you could always email us, but all of our contact information's on that same site.

Stuart: Perfect. I'll put a link to the website in the show notes, so whether people are listening on a podcast player or on the website, they can just click straight through. And I highly recommend people doing that, A, to see what you guys are doing, but also, this idea of the conversation around taking what we know and positioning it for people who we wanna have the conversation with, you've got that on the website.

Stuart: there's resources there that kind of bridge that gap. So again, people might think they know about financial planning and wealth management and not really think about it, but this opportunity to bridge it into your own work, no matter what you do, and think about, okay, who the audience is and what things can I put in front of them that they will resonate with, the website's got some good examples for you and your business.

Stuart: So I'll put the link in there for people.

John Becker: it's not everything, but it's enough to, be at least more educated on what you're doing.

Stuart: Yeah. Conversation starters, yeah ...

John Becker: do, for sure.

Stuart: Yeah, exactly. John, really appreciate your time. It flies by every time I do these podcasts. it'd be good to circle back, as I was saying, the book's just recently, we're wrapping up, so it'd be good to circle back in six months or so and see how it's going with the book particularly and share some updates- Sure

Stuart: with people and do another show.

John Becker: and also, coming up very shortly, we've got the, the second book coming out for our, small business owners, and that one will be with Mr., Robbie Rosenberger and my co-author, Terry George, I believe you're speaking with here shortly for another

Stuart: one. Yeah.

Stuart: Yeah, definitely.

Stuart: So in a week or two we'll have Terry on, and then, we're actually recording tomorrow as we record this one, but it'll be a week or two in the release schedule. So it'll be interesting to almost see it as a counterposition, or not counterposition, but the position of two people doing the same thing and their perspectives on sharing their message.

Stuart: So it'll be an interesting exercise for people listening just to see the different perspectives as well.

Stuart: Yeah, and I think one thing you'll see with Robbie's book, the book we wrote together, there's a lot more human element to the small business book than I think people may think. we even get into the weeds about, the pitfalls of doing business with, family members as partners or as employees, Right.

John Becker: I, I-

Stuart: That could be a whole series by itself.

John Becker: Ooh. Maybe

Stuart: it's- Yeah, you live in interesting times ... wow.

John Becker: All kidding aside though, I think it's just to let people know that we're human, we're not robots, and-

Stuart: Yeah ...

John Becker: there, there is that level of care, but there's also that level of clarity and confidence too.

Stuart: Yeah. Yeah.

John Becker: Those are the big keys.

Stuart: Real people.

John Becker: Caring, confidence, and, it's just... it goes in the name, Clear View.

Stuart: Yeah. Yeah, exactly.

John Becker: Provide people a little bit more clarity on stuff that's really hard to digest on your own.

Stuart: Yeah. Yeah. That supporting part of that, holding people's hands to the extent that they need it.

Stuart: Yeah. Which goes for everyone listening. we all do that in our businesses, John, appreciate it, buddy. I will keep in touch for sure. We'll share some updates with the audience a little bit down the road. And again, just thanks for your time.

John Becker: Thanks, Stuart. Appreciate you.

Stuart: Everyone, thanks for listening.

Stuart: We will catch you all the next one